Adyen – When a Fortress Balance Sheet Hides a Slowing Engine

Adyen still looks like a model fintech company. But the stock has struggled for years while the business continues to grow. That disconnect raises a subtle question investors often overlook.

Before we dive into the analysis I’d like to share a personal thought that is on my mind: this analysis is for you as subscribers and readers, if you find it informative please hit the like button, if you’re missing anything, please leave a comment. It is the only way for me as your author to get feedback and service you in the best way possible.

Back to Adyen!

Can a company look financially strong while its operating momentum quietly weakens?

These signals rarely move in isolation. When read together, they often reveal structural dynamics beneath the surface of a business. (Full framework)

What changed beneath the surface

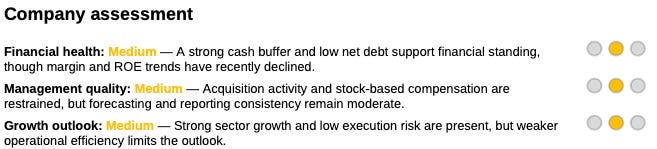

Adyen remains a structurally strong business. Revenue continues to grow as digital payments expand and merchants adopt unified payment platforms, even though growth has recently normalized.

Profitability is still exceptionally high by fintech standards. But the direction of change is more nuanced. Margins have gradually declined from earlier peaks, and return on equity has trended lower, suggesting incremental capital is generating weaker returns than before.

Free cash flow remains strong overall but has become more volatile and recently declined.

At the same time, the balance sheet has strengthened further. Adyen now operates with a large net cash position and virtually no leverage, providing significant financial stability.

The result is an unusual dynamic: operational efficiency is showing early signs of pressure while the balance sheet continues to strengthen.

This situation reflects a recurring financial dynamic: The Balance Sheet Mirage. (See the full pattern here.)

The pattern at work

Why investors often misread this phase and what it implies for valuation

The stock price ultimately reflects a combination of growth, profitability, capital efficiency, and financial risk.

In Adyen’s case, the balance sheet clearly supports valuation. Large cash reserves and minimal leverage reduce financial risk and provide a strong buffer against economic volatility.

However, valuation is not driven by balance sheet strength alone.

Profitability trends, return on capital, and the consistency of cash generation play an equally important role in determining sustainable valuation levels.

This is where the interaction becomes more subtle.

Even though the company remains highly profitable, the gradual decline in margins and returns suggests that the pace of operational improvement may be slowing as shown by the declining fair value band. Meanwhile, volatility in free cash flow introduces greater uncertainty around capital allocation.

In other words, the balance sheet supports stability – but operating trends limit how much valuation can expand. With the stock trading slightly below a falling fair value band, investors should pay attention to the evolution of the underlying metrics.

The insight

Adyen remains a fundamentally strong company.

But the investment dynamic is evolving.

The company is moving from a phase of rapid operational expansion toward a phase where sustaining efficiency becomes more important than simply growing transaction volume.

In this stage of the business cycle, small changes in operating efficiency can matter more than headline growth.

Management quality therefore becomes increasingly relevant. Signals show relatively disciplined acquisition behaviour and limited shareholder dilution, which supports long-term alignment between management and investors.

When a company already operates with a very strong balance sheet, the key question for investors becomes less about financial stability and more about operational discipline.

In other words:

A strong balance sheet protects the company – but only strong execution protects the investment.

Disclaimer: This analysis reflects one recurring structural pattern observed across companies.

To see how financial health, growth, management quality and valuation are evaluated together, explore the Financial X-Ray framework:

This publication is for educational purposes only and reflects analysis of publicly available financial information. It is not investment advice.

Strong point. Investors often treat financial strength as if it automatically makes the investment strong too — but the company and the investment can diverge much earlier than people expect.

I just wrote about it too. I don’t really see it weakening rather it should benefit from scale. Margins should expand a bit still, but valuation anywhere in the 15-20x is likely around fair value